The Highest Economies in the World

When it comes to measuring the economic strength of a country, Gross Domestic Product (GDP) is often used as a key indicator. GDP represents the total monetary value of all goods and services produced within a country’s borders over a specific period of time. Let’s take a look at some of the highest economies in the world based on their GDP:

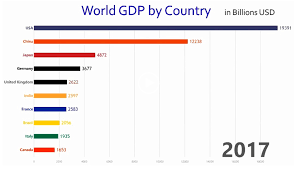

United States

The United States has consistently held its position as the world’s largest economy. With a diverse range of industries including technology, finance, and healthcare, the US GDP continues to grow steadily.

China

China has experienced rapid economic growth over the past few decades, propelling it to become one of the top economies globally. Its manufacturing sector, infrastructure development, and consumer market contribute significantly to its GDP.

Japan

Japan is known for its technological advancements and innovation, which have helped sustain its position as one of the highest economies in the world. Despite challenges such as an ageing population, Japan remains a key player in global trade.

Germany

Germany’s strong industrial base and exports have solidified its status as one of Europe’s leading economies. The country’s emphasis on engineering excellence and innovation continues to drive its economic growth.

India

India’s economy has been on a growth trajectory, fuelled by sectors such as information technology, pharmaceuticals, and services. With a large population and expanding middle class, India is poised to climb higher in global economic rankings.

In conclusion, these top economies play pivotal roles in shaping global trade, investment flows, and economic policies. While each country faces unique challenges and opportunities, their collective impact on the world economy is undeniable.

Strategies for Leading Global Economies: Innovation, Education, Trade, Stability, Diversification, and Fiscal Responsibility

- Focus on innovation and technology to drive economic growth.

- Invest in education and skills training to create a highly skilled workforce.

- Promote international trade and establish strong global partnerships.

- Maintain political stability and a business-friendly environment to attract investments.

- Diversify the economy to reduce dependence on a single industry or sector.

- Implement sound fiscal policies and efficient public administration for sustainable economic development.

Focus on innovation and technology to drive economic growth.

In today’s competitive global landscape, focusing on innovation and technology is paramount to driving economic growth for the highest economies in the world. Embracing cutting-edge technologies and fostering a culture of innovation not only enhances productivity and efficiency but also opens up new avenues for sustainable development. By investing in research and development, nurturing entrepreneurial talent, and adapting to digital transformation, countries can position themselves as leaders in the ever-evolving global economy. Innovation and technology serve as catalysts for progress, enabling nations to stay ahead of the curve and shape a prosperous future for their citizens.

Invest in education and skills training to create a highly skilled workforce.

Investing in education and skills training is a crucial strategy for countries aiming to strengthen their position among the highest economies in the world. By prioritising the development of a highly skilled workforce, nations can enhance productivity, foster innovation, and drive economic growth. Equipping individuals with relevant knowledge and expertise not only benefits the workforce but also boosts overall competitiveness in the global market. Education and skills training lay the foundation for sustainable economic progress, empowering individuals to adapt to evolving industries and technologies, ultimately contributing to the prosperity of a nation’s economy.

Promote international trade and establish strong global partnerships.

Promoting international trade and fostering strong global partnerships are essential strategies for countries aiming to strengthen their position among the highest economies in the world. By engaging in trade agreements and collaborations with other nations, countries can access new markets, attract investments, and enhance economic growth. Building robust global partnerships also facilitates the exchange of knowledge, technology, and resources, leading to mutual benefits and sustainable development. Embracing a proactive approach towards international trade and cooperation not only boosts a country’s economic standing but also fosters diplomatic ties and cultural exchange on a global scale.

Maintain political stability and a business-friendly environment to attract investments.

Maintaining political stability and fostering a business-friendly environment are crucial factors in attracting investments to sustain and grow a country’s economy. Political stability provides a sense of security for investors, ensuring that their investments are protected from abrupt policy changes or unrest. A business-friendly environment, characterised by transparent regulations, efficient bureaucracy, and incentives for businesses, encourages both domestic and foreign investors to allocate capital and resources into the economy. By prioritising these aspects, countries can create an environment conducive to economic growth, job creation, and overall prosperity.

Diversify the economy to reduce dependence on a single industry or sector.

In light of the ranking of the highest economies in the world, a crucial tip emerges: diversifying the economy can mitigate risks associated with over-reliance on a single industry or sector. By broadening the range of industries and services within a country’s economic landscape, nations can enhance resilience to market fluctuations and external shocks. This strategy not only fosters sustainable growth but also promotes stability and long-term prosperity by spreading risk across multiple sectors. Embracing economic diversification can pave the way for a more robust and adaptable economy, less vulnerable to disruptions in any single industry.

Implement sound fiscal policies and efficient public administration for sustainable economic development.

Implementing sound fiscal policies and efficient public administration are crucial steps towards achieving sustainable economic development in the highest economies of the world. By ensuring that government spending is responsible and aligned with long-term economic goals, countries can maintain stability and promote growth. Efficient public administration helps to streamline processes, reduce bureaucratic inefficiencies, and enhance transparency, which are essential for attracting investments and fostering a conducive environment for businesses to thrive. Through these measures, economies can build a solid foundation for sustainable development that benefits both current and future generations.